the mean reversion imps

an addition to the bestiary

(Content note: sorry! The Friday post last week didn’t materialise and this is a day late. I’m trying to get back on track). Anyway …

Befitting its ancient and mythical status, the British economy is, as can be confirmed by reading journalism on the subject, basically a realm of fantasy. We all mourn the disappearance of the “magic money tree”, and some of us believe that it might still exist, hidden in Threadneedle Street. The Reform Fairy determines long term public spending growth, while the Confidence Fairy sets the level of long term interest rates and the exchange rate.

However, possibly hidden away in the Celtic Fringes, I think there’s another kind of mythical wee beastie which is about to become important.

One of my former colleagues, who was more of an intellectual than he liked to pretend to be, used to say that there are really only two methods of forecasting – extrapolation of a trend, or mean reversion. There’s a lot of truth to that in all honesty, as a great deal of the methodology of statistical prediction is basically about identifying and extracting trends, then analysing the drivers of the deviations from those trends, which are presumed to be stationary.

“Stationary” is a term of art here which I’m not going to unpack too much because to do so would involve a real digression. But for the time being I’ll point out that “mean reversion”, in the loose sense I’m using it here, is ambiguous.

It might refer to a situation in which there’s an actual mechanism which drags things back toward a particular long term level, where you can expect oscillation around a long term norm. Think, maybe, of profit margins in an industry, where shortages lead to gluts and vice versa. Or it might just mean “regression to the mean”, the fact that if you know that a process is stationary then lower values are more likely to be followed by higher ones than by even-lower ones. (What am I on about? Think of the TV show “Play Your Cards Right”. The cards are random, but if the host turns over the three of clubs, you are better off saying “Higher” than “Lower”. That’s called “regression to the mean” for annoying historical reasons which don’t tell you anything about the problem).

So anyway – the reason that this is on my mind is that a lot of people tend to assume that productivity growth (the annual change in output per worker-hour, which we economists heroically assume to be representing the limitless Whiggish march of technological progress) is in some way a mean-reverting process. Specifically, that it reverts to a trend which, since the war, seems to correspond to roughly two per cent real GDP growth per year. Why? Economists tend to put it down to technological progress, but personally I think it’s more likely to be pixies.

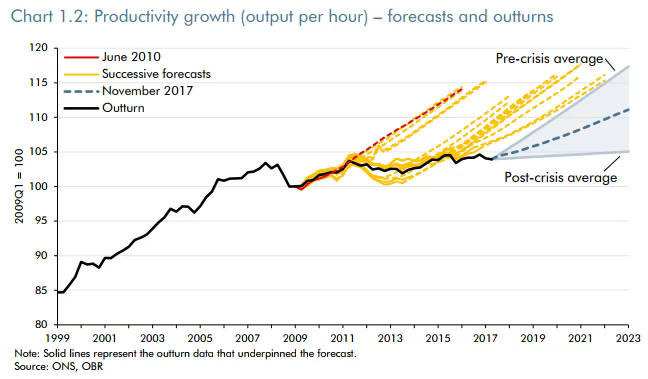

Trouble is, this productivity trend used to be a very well-established empirical fact, but then it ceased to be so. Basically, there have always been temporary deviations from the trend associated with booms and busts in the business cycle, but the deviation in the great financial crisis in 2008 never got mean-reverted. Instead – well, look at this chart, which also shows the expectation of the consensus of mainstream economic thought, as summarised by the Office of Budget Responsibility, that the mean reversion imps would come along to do their stuff.

Something has gone on here, it would appear. Getting into questions of policy and structure is definitely beyond the scope of this post, so let’s presume for the moment I’m right and the problem with the series is simply a lack of activity on the part of the relevant supernatural woodland spirits. There’s basically three possibilities:

1) This is the new normal, we’ve mortally offended the pixies and the new trend rate of productivity growth is much lower forever.

2) We just had a run of bad luck with the pixies; there’s no particular reason to believe that they won’t come back really soon and we’ll go back to the good old 2% a year.

3) Same as 2), but when the pixies come back, they will realise that they’ve been slacking on the job and we’ll have to have a period of higher growth to get us back to the trend.

You can tell various stories with more economic content to them obviously, but I think it’s important to be clear here that the really optimistic 3) is not at all something you can rule out as nonsense. If a country has, for one reason or another, fallen a long way behind the maximally efficient frontier, then it’s perfectly reasonable to expect a period of “catch-up” growth, as there is more low-hanging fruit around in the form of good investments which should have been made but weren’t.

The argument for the pessimistic 1), on the other hand, is really mainly “look at the bloody state of this bloody forecast chart”, which might gain some credibility from the very fact that there’s not much economic content to it. And in fact, as you can see, after years of being disappointed and ridiculed, the OBR have started shading their forecasts downward.

This matters to me because I think it’s quite likely that our Chancellor believes in mean reversion pixies. Partly because, as I say, the theory of productivity as a trend-reverting process is quite orthodox (for the heads, it’s known as “the unit root debate”, for even more annoying historical reasons that don’t tell you anything at all about the problem than “regression to the mean”). If one takes Napoleon’s maxim seriously that to understand someone’s worldview you need to think about what the world was like when they were in their early twenties, then this was, I think, the house view of Former Bank of England Economists at the start of the century.

And also, obviously, there’s the potential for motivated reasoning. If you’ve talked yourself into a corner with respect to fiscal rules and you’ve promised not to raise the big taxes that could make a difference, then you’re stuck into a model of growth that I’ve described as “returns first, investment later”. This is very likely to result in a trap of failing public infrastructure … unless something turns up and economic growth picks up of its own accord. Which is what you’d expect if you’re anticipating that the mean reversion pixies are still out there, just waiting for Liz Truss and Kwasi Kwarteng to stop scaring them away.

It's not in any way a ridiculous thing to believe and it might not even be wrong. It just worries me that it’s so damned congenial for an optimist.

I think there's also a third kind of forecast, leaving us with:

- things will stay the same as they are now

- things will keep changing the way they've been going

- things will go back to how they were

The same question arises in relation to output growth and recessions. The standard view is (3), return to long run trend, but the evidence is more supportive of (2). For example, in looking at the divergence between Australia and New Zealand since 1980, the best explanation is that New Zealand has had more and deeper recessions. For those who aren't aware, NZ invented inflation targeting around 1990